Note

The Medigap policy covers coinsurance only after you’ve paid the deductible

(unless the Medigap policy also pays the deductible).

Let’s get started by looking at the chart with detailed explanation of the various parts of the chart.

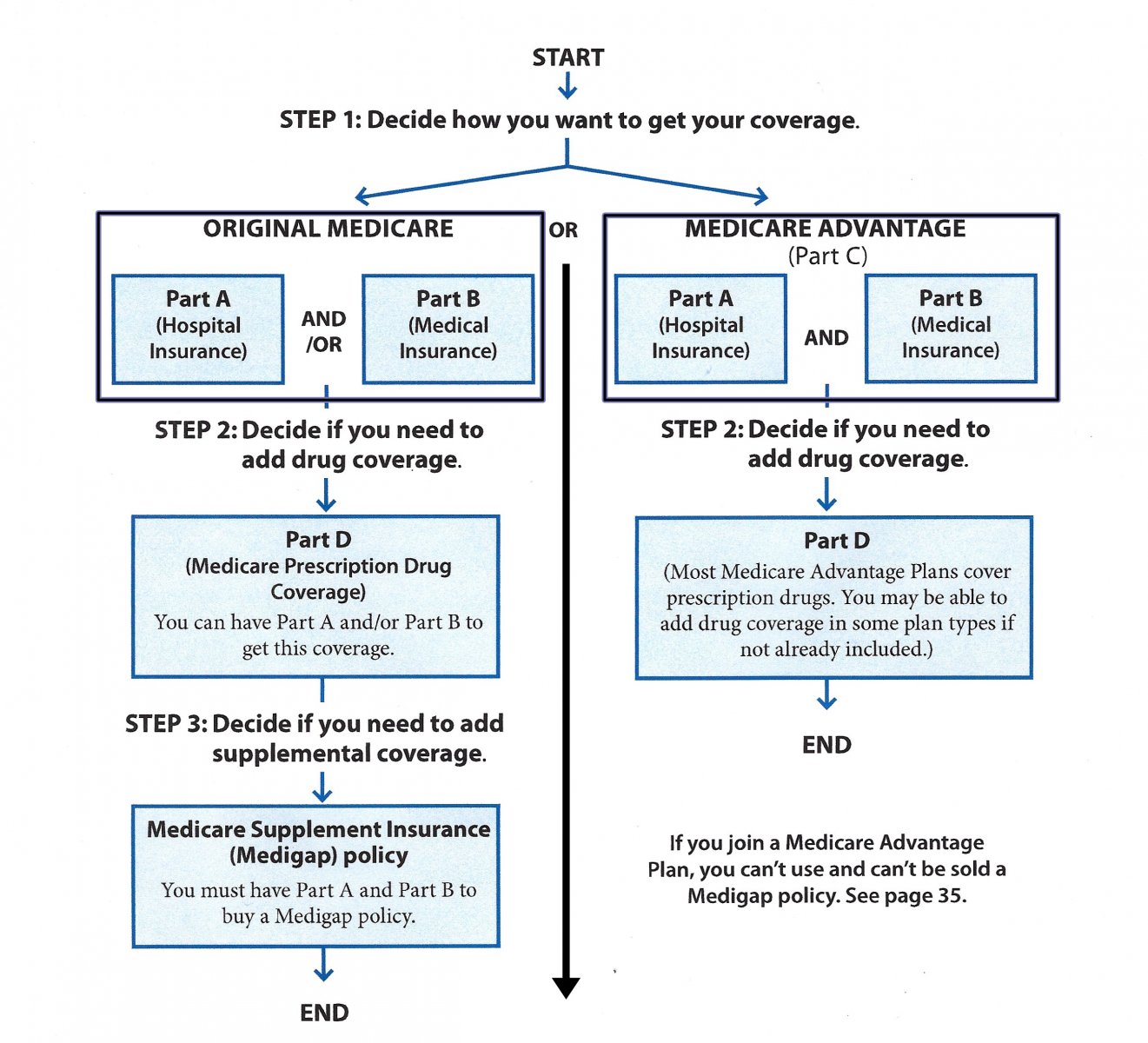

Looking at this chart there are two major directional choices you must make either when you first sign up for Medicare or during the open enrollment. And if you’re considering changing your plan during open enrollment, or at least exploring your options, this information will be most helpful.

When you turn 65, or whenever you receive your Medicare card, you are eligible for Part A of original Medicare. If you have also enrolled in Part B, which would be indicated on your Medicare card, then you have both Part A and Part B Medicare insurance.

Let’s take a look below at the Left side of this chart which is Original Medicare.

Part A hospital insurance is automatically covered under original Medicare. Part B medical insurance is an option you have, but you must pay a Part B premium each month. This part B premium can be deducted from your Social Security if you take Social Security at age 65, or it can be separately billed to you. Most people sign up for part B medical insurance benefit when they turn 65. If you do not sign up for part B, unless you’re covered under a qualified Medicare plan through a group policy from your employer, and later decide to sign up for part B you will most likely incur a penalty which would be an additional charge to your part B premium.

So, if you choose to keep your original Medicare benefit with Part A and Part B, you will be covered approximately 80% (based on average) of your health care costs except for prescription drugs.

To have prescription drug coverage, private insurance plans called Medicare Part D Prescription Drug Plans, are available from private insurance companies with a monthly premium. Without this separate private insurance Part D Prescription Drug Plan, you will not have prescription coverage. Note: there are private Internet and pharmacy plans that provide some discounts from retail prices of prescriptions. But I recommend a Part D Prescription Drug Plan as a better way to same on prescriptions.

Continuing on the left side of original Medicare, you have one more option. That option is to add a Medicare Supplement Insurance (Medigap) Policy from a private insurance company. This is not part of Original Medicare but in addition to Original Medicare furnished by private insurance companies. Both Part D Medicare Prescription Drug plans and Medicare Medigap Supplement Insurance policies are provided by private insurance companies.

Below is a summary of the plans in \ Medigap Supplement Insurance:

Every Medigap policy must follow federal and state laws designed to protect you, and it must be clearly identified as “Medicare Supplement Insurance.” Insurance companies can sell you only a “standardized” policy identified in most states by letters.

All policies offer the same basic benefits but some offer additional benefits, so you can choose which one meets your needs. In Massachusetts, Minnesota, and Wisconsin, Medigap policies are standardized in a different way.

Each insurance company decides which Medigap policies it wants to sell, although state laws might affect which ones they offer. Insurance companies that sell Medigap policies:

Note

The Medigap policy covers coinsurance only after you’ve paid the deductible

(unless the Medigap policy also pays the deductible).

The chart below from shows basic information about the different benefits Medigap policies cover.

Yes = the plan covers 100% of this benefit

No = the policy doesn’t cover that benefit

% = the plan covers that percentage of this benefit

N/A = not applicable

| Medigap Benefits | Supplement (Medigap) Plans | |||||||||

| A | B | C | D | F* | G* | K | L | M | N | |

| Part A coinsurance and hospital costs up to an additional 365 days after Medicare benefits are used up. (You might pay a premium if you only have 39 quarters or less in Medicare taxes) | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Part B coinsurance or copayment | Yes | Yes | Yes | Yes | Yes | Yes | 50% | 75% | Yes | Yes*** |

| Blood (first 3 pints) | Yes | Yes | Yes | Yes | Yes | Yes | 50% | 75% | Yes | Yes |

| Part A hospice care coinsurance or copayment | Yes | Yes | Yes | Yes | Yes | Yes | 50% | 75% | Yes | Yes |

| Skilled nursing facility care coinsurance | No | No | Yes | Yes | Yes | Yes | 50% | 75% | Yes | Yes |

| Part A deductible $1,600 | No | Yes | Yes | Yes | Yes | Yes | 50% | 75% | 50% | Yes |

| Part B deductible $233 | No | No | Yes | No | Yes | No | No | No | No | No |

| Part B excess charge | No | No | No | No | Yes | Yes | No | No | No | No |

| Foreign travel exchange (up to plan limits) | No | No | 80% | 80% | 80% | 80% | No | No | 80% | 80% |

| Out-of-pocket limit** | N/A | N/A | N/A | N/A | N/A | N/A | $7,060 | $3,530 | N/A | N/A |

| * Plans F and G also offer a high-deductible plan in some states. With this option, you must pay for Medicare-covered costs (coinsurance, copayments, and deductibles) up to the deductible amount of $2,700 for 2023 before your policy pays anything. (Plans C and F aren’t available to people who were newly eligible for Medicare on or after January 1, 2020.) | ||||||||||

| ** For Plans K and L, after you meet your out-of-pocket yearly limit and your yearly Part B deductible, the Medigap plan pays 100% of covered services for the rest of the calendar year. | ||||||||||

| *** Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in inpatient admission. | ||||||||||

Starting January 1, 2020, Medigap plans sold to new people with Medicare won’t be allowed to cover the Part B deductible. Because of this, Plans C and F will no longer be available to people new to Medicare starting on January 1, 2020. If you already have either of these 2 plans (or the high deductible version of Plan F) or are covered by one of these plans before January 1, 2020, you’ll be able to keep your plan. If you were eligible for Medicare before January 1, 2020, but not yet enrolled, you may be able to buy one of these plans.

For many Medicare clients, an Advantage Plan might be a better option.

When you choose an Advantage plan, you are leaving the Government financed Original Medicare plan for an Advantage Plan that is financed by private insurance companies. You must have both PART A and PART B in order to apply for a Medicare Advantage Plan. The private insurance company receives from the government a portion of all of your premium for your Advantage Plan. In many cases your monthly Advantage Plan premium is very low and sometimes even at zero premium that you have to pay.

One other point about Advantage plans. Most plans include prescription drug coverage. However, there are some plans that do not cover prescription drugs. Therefore, you may want to enroll in a Medicare Advantage Prescription Drug plan (MA-PD).

When prescriptions are not included in an Advantage plan, and you want to have prescription coverage, a separate Part D Prescription Drug Plan must be purchased. This is optional. It is not required that you purchase a Part D plan, only if you want prescription coverage.

Remember most advantage plans include prescription drug coverage. Just make sure the plan you are considering includes this coverage.